Precision Agriculture Robotics

By an AgTech Analyst with over a decade tracking automation across the U.S. farm belt

Here’s a number that stopped me cold: by 2033, the precision agriculture robotics market is projected to hit somewhere between $38 billion and $148 billion depending on which analysts you believe. That’s not a rounding error. That’s a sign that something fundamental has shifted in how we grow food.

Precision agriculture robotics is the integration of autonomous machines, AI-driven sensors, and real-time data systems to perform targeted farming tasks planting, weeding, spraying, monitoring, and harvesting with accuracy that human hands simply can’t match at scale. It’s not science fiction. It’s happening right now on farms across the American Midwest, in vineyards across California, and in greenhouses from the Netherlands to India.

And yet most coverage of this topic either drowns you in jargon or stays so surface-level it’s useless. Let’s fix that.

Why U.S. Farms Are Running Out of Time (And Workers)

The agricultural labor crisis isn’t coming. It’s already here.

The U.S. agricultural robots market reached $3.1 billion in 2024, and the primary driver isn’t tech enthusiasm it’s desperation. Farms across the country are struggling to find enough workers to pick, plant, and maintain crops at the pace the market demands. Aging rural workforces, rising H-2A visa costs, and post-pandemic labor dynamics have pushed the problem past a tipping point.

I talked to a mid-sized strawberry grower in Watsonville, California, back in 2023. He’d been farming for 30 years. “We had 40% fewer pickers show up last season than we needed,” he told me. “I can’t grow more fruit if I can’t get it off the vine.” That’s not a unique story anymore it’s the norm.

Walt Duflock, VP of Innovation at Western Growers, put it plainly: automation is “a complement to the labor they have trouble finding and continues to go up in cost every year.” He wasn’t talking about replacing people. He was talking about survival.

The global precision farming market was valued at $10.5 billion in 2024 and is estimated to grow at a CAGR of 11.5% through 2034, driven largely by food demand pressure. The United Nations projects world population will reach 9.8 billion by 2050, which means crop demand needs to rise by roughly 60% without necessarily expanding the amount of farmable land. Something has to give. Robotics is increasingly that something.

Variable rate technology alone already reduces fertilizer usage by up to 20%, while real-time irrigation scheduling cuts water use by up to 30%. Those aren’t marginal gains. On a 2,000-acre operation, that’s real money.

How Precision Agriculture Robots Actually Work: A 4-Stage Field Cycle

Most articles describe robotic farming in abstract terms. Here’s what the actual field workflow looks like in 2025.

Stage 1: Sensing and Data Collection

Before any robot does anything physical, sensors do the talking. Agricultural robots are equipped with multispectral and hyperspectral cameras that analyze plant health using indices like NDVI (Normalized Difference Vegetation Index), plus environmental sensors that detect soil moisture, temperature, and chemical composition.

Drones fly prescribed grid patterns, capturing data that would take a human crew weeks to gather manually. The result is a granular, real-time map of the entire field which areas are water-stressed, which patches show early signs of disease, where nutrient deficiencies are developing before they become visible to the eye.

Stage 2: AI-Driven Decision Making

Raw sensor data is useless without interpretation. Machine learning models analyze data from IoT sensors and historical records to predict optimal planting, irrigation, and harvesting times, helping farmers minimize waste, optimize labor, and increase crop yields.

This is where modern precision agriculture robotics separates itself from earlier automation. A GPS-guided tractor in 2005 followed a path. A 2025 autonomous system makes decisions adjusting application rates mid-row, flagging anomalies for human review, rerouting around wet spots to prevent soil compaction.

Stage 3: Targeted Action

Here’s where the payoff happens. Ecorobotix launched the ARA Ultra-High Precision Field Sprayer in February 2025, featuring AI-based Plant-by-Plant technology that results in up to a 95% reduction in chemical use. Not 10%. Not 30%. Ninety-five percent, by targeting each individual plant rather than blanket-spraying entire rows.

Weeding robots can precisely target weeds, reducing herbicide application by up to 90% compared to traditional methods. The machines don’t get tired. They don’t accidentally spray the wrong zone. They don’t take a lunch break when the window of optimal treatment is narrow.

Stage 4: Continuous Learning and Feedback

The best robotic systems improve with every pass. Reinforcement learning algorithms adjust robot behavior based on outcomes a harvesting robot that was too aggressive with ripe tomatoes last Tuesday will apply lighter grip pressure this Tuesday. That compounding improvement is something traditional mechanization never offered.

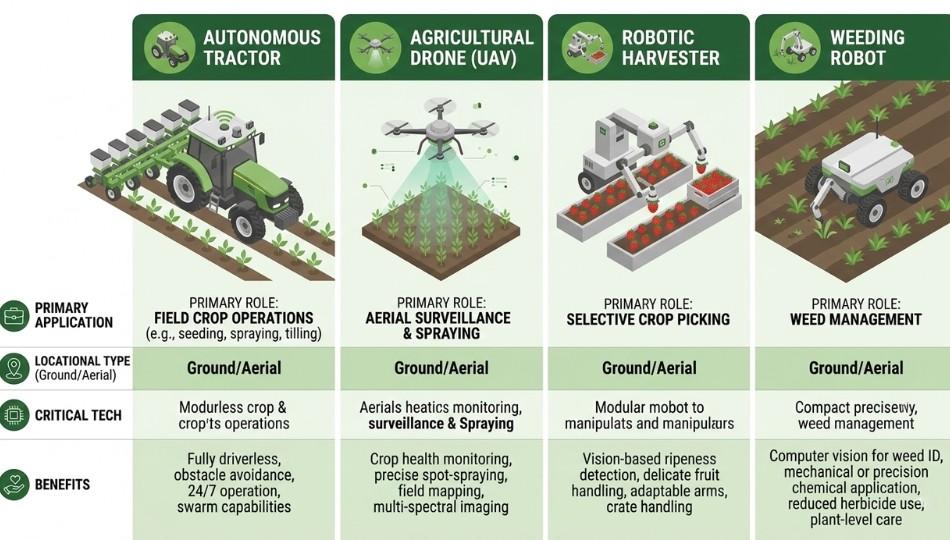

Autonomous Tractors vs. Drones vs. Robotic Harvesters: Which Actually Delivers ROI?

This is the question nobody’s asking clearly enough and the answer isn’t the same for every farm.

Autonomous Tractors

Driverless tractors from companies like John Deere and CNH Industrial are the workhorses of large-scale grain operations. They’re best suited for flat, open-field environments corn, soybeans, wheat. The ROI case is straightforward: one operator can supervise multiple machines simultaneously, dramatically reducing labor costs per acre during planting and harvest windows.

But don’t assume they’re universally applicable. Hilly terrain, irregular field shapes, and specialty crops make fully autonomous navigation far more complex and expensive. (Yes, I’ve seen demos where the tech struggled on anything more challenging than Kansas.)

Agricultural Drones (UAVs)

UAVs are expected to hold the highest market share going forward, and it’s not hard to see why. The barrier to entry is lower, the flexibility is higher, and the applications span almost every crop type. Drones handle soil and crop monitoring, precision spraying, and even direct seeding in some applications.

An estimated 50% of farmers are expected to be using data analytics platforms by 2025, and drones are one of the primary data-gathering tools feeding those platforms. For a smaller operation that can’t justify a $500,000 autonomous tractor, a $15,000 agricultural drone paired with good software might deliver the highest near-term ROI.

Robotic Harvesters

This is where the technology is most impressive and most uneven. Tortuga AgTech in Colorado has built robots that use computer vision and machine learning to pick strawberries and table grapes with precision comparable to human pickers. Similar systems are emerging for citrus, apples, and salad greens.

Farms using robotic weeding systems reduced weeding costs for high-density crops by 40%, and were able to reallocate workers to harvesting a critical point that gets missed in most coverage. Robotics doesn’t always eliminate jobs outright. Often it redistributes labor toward tasks that require more human judgment.

The honest comparison:

| Robot Type | Best For | Upfront Cost Range | Key ROI Driver |

|---|---|---|---|

| Autonomous Tractor | Large grain/row crops | $250K–$600K | Labor reduction, fuel efficiency |

| Agricultural Drone | Any crop size, monitoring + spraying | $5K–$50K | Input savings, early detection |

| Robotic Harvester | Specialty crops, fruits | $100K–$400K+ | Labor shortage mitigation |

| Weeding Robot | High-density row crops | $50K–$250K | Chemical cost reduction |

The Real Outcomes: What Precision Agriculture Robotics Does for the Bottom Line

Let’s be direct about what this technology actually delivers in practice not in press releases.

The global agricultural robots market was estimated at $14.74 billion in 2024 and is projected to reach $48.06 billion by 2030, growing at a CAGR of 23%. That growth rate only happens when buyers are seeing real returns.

The wins are clearest in three areas. First, input cost reduction robotics cuts chemical, water, and fertilizer use through precision application, not guesswork. Second, labor cost stabilization farms using automation can plan operations without the anxiety of not knowing if pickers will show up. Third, yield quality improvement. Automated harvesting machines operate continuously without fatigue, collecting crops at peak ripeness. That’s not just better produce it extends shelf life and improves buyer prices.

Here’s the angle most articles skip: robotics also changes risk profiles. A farm without automation is vulnerable to weather windows and labor availability simultaneously. A farm with autonomous systems running during overnight hours or through light rain events can recover from scheduling setbacks that used to cost entire harvests.

Who does this work for? Large operations with capital to invest, specialty crop growers facing acute labor shortages, and increasingly thanks to declining hardware costs and robot-as-a-service (RaaS) models mid-sized farms that would never have considered it five years ago.

Who should pump the brakes? Very small diversified farms, operations in regions with abundant affordable labor, and any farm without reliable connectivity infrastructure. Autonomous systems need data pipelines. If your fields are in a dead zone, the ROI math changes significantly.

Expert Perspective

Researchers from Springer Nature’s Discover Robotics journal note that autonomous robotics “plays a central role in the development of precision agriculture” and that the combination of mobile robotics, machine vision, and advanced sensors is “revolutionizing crop management, reducing environmental impact and increasing yield.” Their analysis, published in July 2025, frames this as “not just machine automation but a true transformation combining efficiency, sustainability, and technological innovation.”

That framing matters. The conversation in 2025 has moved past “will robots replace farmers?” toward “how do farmers and robots divide the work more intelligently?” The evidence suggests the answer is showing up in input cost data, yield reports, and increasingly, in farm profitability figures.

Three Things Worth Knowing Before You Act

After watching this market evolve through boom cycles and overhyped demos, here’s what actually matters right now.

First: the best entry point for most farms isn’t a $400,000 autonomous harvester. It’s data. Start with drones and sensors that tell you what’s actually happening in your fields. The decision-making upgrade comes before the physical robot upgrade.

Second: the labor math has already shifted permanently. The agricultural workforce was contracting before COVID, and post-pandemic trends haven’t reversed. Precision agriculture robotics isn’t something to evaluate “eventually” it’s something to plan for in your next capital cycle.

Third: don’t let perfect be the enemy of good. The robots available today aren’t perfect. They have terrain limitations, connectivity dependencies, and maintenance curves. But farms that started experimenting with autonomous weeding and UAV monitoring three years ago are now operating with compounding advantages over competitors who waited.

Whether you’re managing 200 acres of specialty crops or 5,000 acres of row crops, precision agriculture robotics is no longer a niche investment. It’s becoming the baseline for staying competitive.

Ready to go deeper? Explore the USDA’s Agricultural Research Service resources on farm automation, or connect with your state’s land-grant university extension program most now have dedicated precision ag specialists who can assess your specific operation.

Frequently Asked Questions

Precision agriculture robotics refers to autonomous and semi-autonomous machines that use sensors, AI, GPS, and computer vision to perform targeted farming tasks planting, spraying, weeding, monitoring, and harvesting with high accuracy. The goal is to apply the right input, at the right location, at the right time, reducing waste and improving yields.

Entry-level agricultural drones start around $5,000–$15,000, making them the most accessible option for smaller operations. Weeding robots and autonomous sprayers typically run $50,000–$250,000. Many startups now offer robot-as-a-service (RaaS) models, where farms pay per acre rather than buying equipment outright, significantly lowering the barrier to entry.

Yes, dramatically. AI-guided spraying systems like Ecorobotix's ARA achieve up to 95% reduction in chemical use through plant-by-plant targeting. Even more conventional robotic weeding tools reduce herbicide application by 60–90% compared to blanket-spray methods.

Specialty crops strawberries, grapes, tomatoes, citrus, lettuce benefit most due to acute labor shortages and high per-acre value. Large row crops like corn and soybeans benefit most from autonomous tractors and monitoring drones. Dairy operations are also heavy adopters, with robotic milking systems dominating a large segment of the market.

For most mid-to-large operations facing labor uncertainty, the answer is trending toward yes especially as hardware costs decline and RaaS models spread. Variable rate technology reduces fertilizer costs by up to 20%; robotic irrigation saves up to 30% on water. Those savings compound annually against a one-time capital deployment.

High upfront costs, connectivity requirements, terrain limitations, and the need for technical skills to operate and maintain systems are the main barriers. Many farmers, especially at the local level, lack training to handle troubleshooting and data analysis, which slows adoption on smaller operations.

AI powers navigation, object recognition (distinguishing crops from weeds), predictive analytics for planting and harvesting timing, disease and pest detection from camera data, and adaptive behavior robots that improve their own technique based on real-time feedback and historical performance data.

Strong. The market is projected to grow at CAGRs ranging from 12% to 23% depending on the segment, driven by rising food demand, shrinking agricultural labor supply, falling hardware costs, and increasing government support for smart farming initiatives. North America currently leads adoption, but Asia-Pacific is projected to grow fastest in the next decade.